Road user charging for light vehicles in Australia

12 June 2019

Road user charging is a potential approach to taxation which involves charging vehicle users per unit of distance travelled. It has become a common topic of discussion in transport policy in Australia and is being considered by various governments. It is often reported in the media that declining fuel excise revenue is a justification for moving to a distance-based road user charge. However, the perception of an oncoming road funding shortfall is exaggerated, and a road user charge may not be the best possible solution. Given this, policy makers should consider the other potential applications of a road user charge, particularly as a mechanism to reduce congestion.

It is often reported in the media that declining fuel excise revenue is a justification for moving to a distance-based road user charge. Several media commentators have suggested that increases in vehicle fuel efficiency will result in “a multi-billion-dollar road funding black hole”[1], or that “fuel excise revenue is in rapid and terminal decline”[2]. As a result, it is often inferred that the Commonwealth will be unable to fund the infrastructure investment needed to support Australia’s growing population and economy. The Commonwealth has also made a similar argument for a distance-based road user charge on light vehicles.[3]

In relation to charging light vehicles, the perception of an oncoming funding shortfall is exaggerated. Fuel excise revenue actually increased in 2016-17 and may continue to do so in the short term due to re-indexation. Furthermore, due to the nature of consolidated revenue and Government budgeting processes, it is unlikely that we will reach the point where we run out of funds to support infrastructure development.

In this article, I will provide a brief discussion of the road user charging reforms for light vehicles, with a particular focus on the relationship between road user charging, fuel excise revenue and infrastructure expenditure. I will briefly describe the current system of road related revenue and expenditure and provide an overview of recent Commonwealth efforts in this space.

Commonwealth policy and road related revenue

Road user charging for light vehicles took a major step into the public sphere in November 2017 when the then Minister for Urban Infrastructure, Paul Fletcher, announced that the government would undertake a study into the implications of road user charging for light vehicles.[4] Up to this point, the majority of Commonwealth efforts on road user charging had focused on reforming heavy vehicle charging arrangements.[5] While the study into light vehicles has not yet eventuated[6], publicly available articles do provide some insight into the Commonwealth’s approach to this issue.

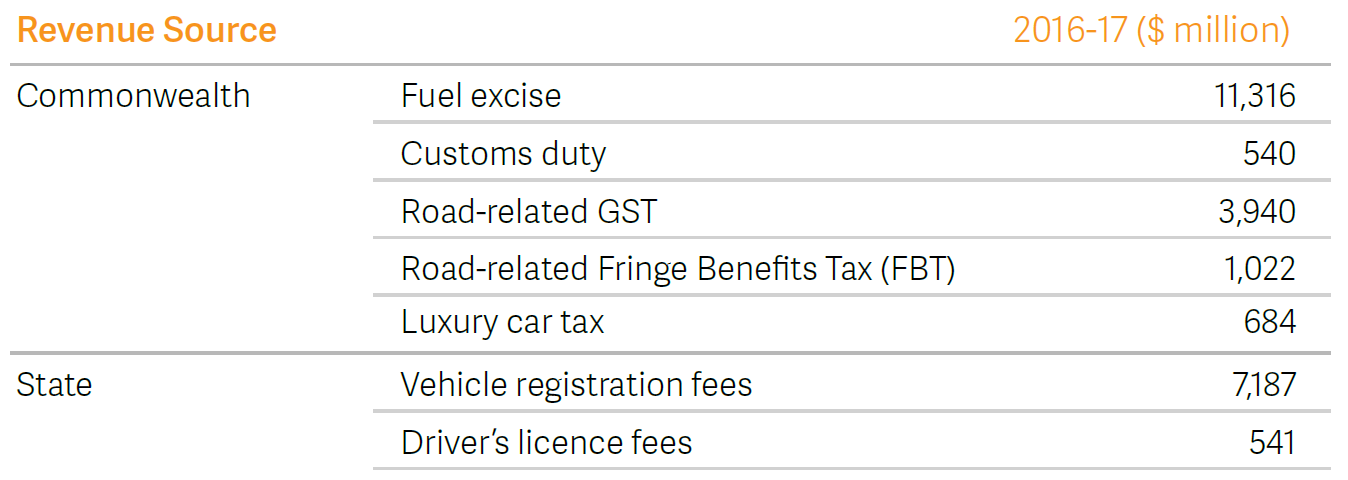

The Commonwealth’s narrative for pursuing road user charging for light vehicles has often focused on ensuring there is a sustainable flow of revenue that can underpin future investment in road infrastructure.[7] In Australia, revenue is collected from a variety of road related activities as shown in Table 1.[8]

Table 1: Select road related revenue sources

The largest of these is fuel excise, followed by vehicle registration fees. The fuel excise quoted above is net of fuel tax credits and off-road usage, so it represents the amount of funds which the Federal Government collects and is able to spend on services.[9] Fuel excise is a fixed charge paid per litre of fuel. The current rate is 41.6 cents per litre.[10] When a driver purchases fuel at a petrol station, this charge is included in the price.

Funding sustainability as a motivation for a road user charge

Australia’s growing population is expected to require greater spending on infrastructure to facilitate more travel demand. In addition, expected growth in electric vehicles and fuel efficiency will reduce fuel excise revenue per kilometre travelled. Thus, it seems plausible that declining fuel excise revenue will make it difficult for governments to invest in the infrastructure that is needed to support Australia’s growing population.

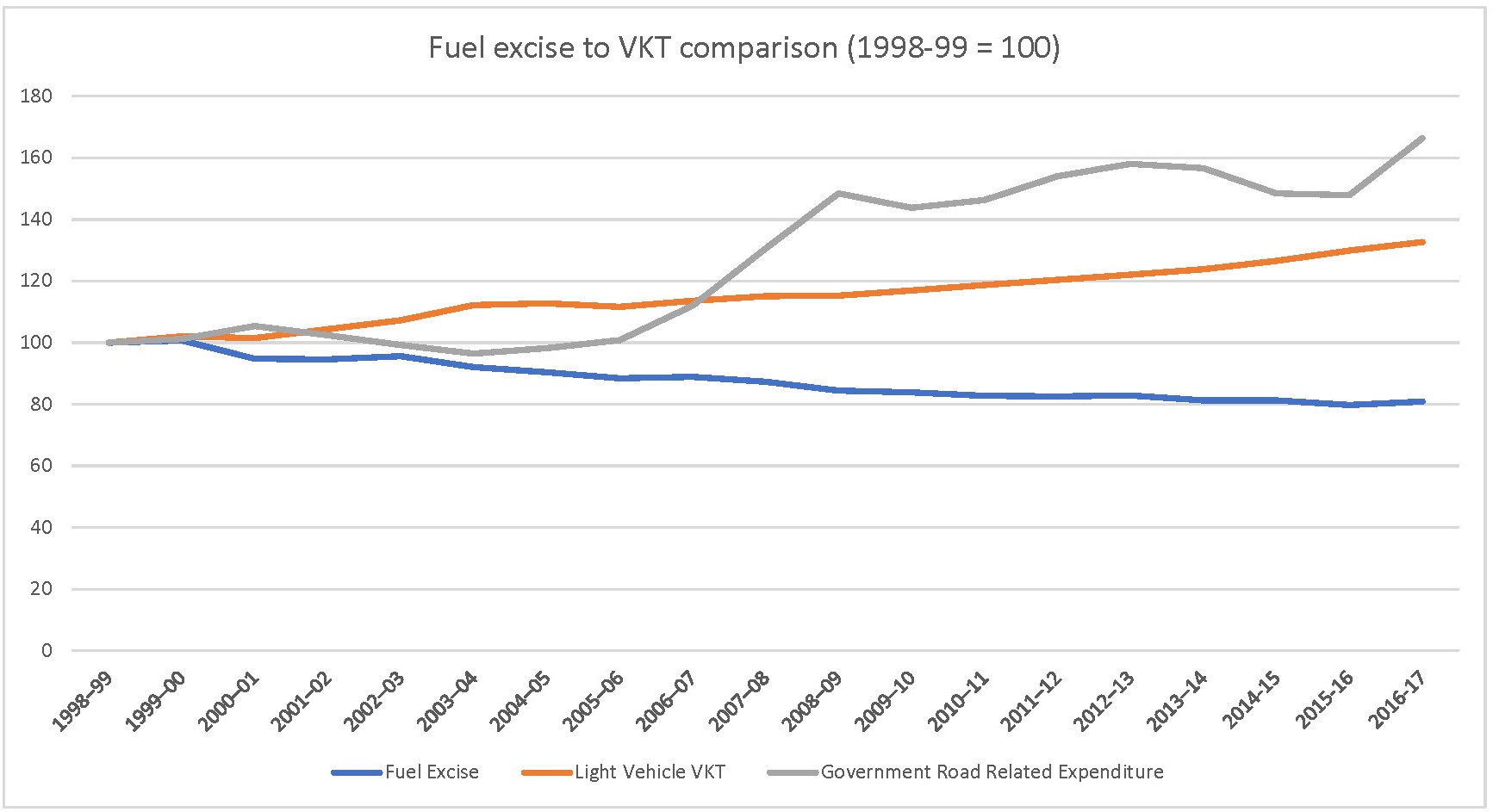

This is summarised in Figure 1 which shows fuel excise revenue, all government (state, local and Federal) expenditure on roads and vehicle kilometres travelled (VKT – light vehicles only – motor cycles, cars and light commercial vehicles) indexed to 1998-99.[11] As can be seen, since 1998-99, road related expenditure by governments has increased by approximately 60 per cent, VKT by light vehicles has increased almost 40 per cent, yet fuel excise revenue has declined by around 20 per cent.

Figure 1: Comparison of net fuel excise revenue, VKT and road related expenditure

This evidence underpins the motivation for adopting a road user charge. Essentially, without charging road users based on their road usage, road related revenues will fall below the amount required to deliver road infrastructure to the general population.

While this view seems intuitive, there are a few additional factors to consider. Firstly, in 2014 fuel excise indexation was (re)introduced[12], whereby the fuel excise per litre charge is increased by CPI biannually. This has resulted in net-fuel excise increasing over 2015-16 to 2016-17 by around $150 million.[13] Furthermore, it is likely that we will see this trend increase over the short term due to the positive impact of indexation. So, while the currently available data does indicate a decline in fuel excise, this obscures the positive impact of indexation on revenue. It is unfair to say, as some commentators have, that there is “a multi-billion-dollar road funding black hole”[14], or “fuel excise revenue is in rapid and terminal decline”[15].

The second thing to note is that ‘road related revenue’ is merely revenue collected from road related sources. Governments are not required to spend road related revenue on roads. Rather, this revenue, alongside most other government revenue, is placed in ‘consolidated revenue’ which is a pool of revenue collected by the government. Consolidated revenue is then used by the government to meet its expenditure as required – including roads, schools or hospitals.

As the government funds roads using consolidated revenue, a decline in road related revenue does not necessarily mean that the government cannot meet its required expenditure on roads – it could draw on revenue collected from other activities or it could raise taxes in some other sector to offset fuel excise decline. It could also reprioritise its spending in other areas. The Grattan Institute have made this point previously in their discussions of road user charging.[16]

While revenue sustainability is a commonly raised issue, there is another issue here – fairness.[17] With the advent of electric and other alternative fuel vehicles, there will be a growing number of vehicles that pay little or no fuel excise. While the loss of revenue to the government may not create an infrastructure funding black hole, it remains an open question as to why these vehicles should not pay fuel excise, or possibly a distance based equivalent charge which contributes to covering their cost for using public roads.[18] This is a complex issue that was raised again recently by Infrastructure Partnerships Australia who emphasise that this is an issue that should be dealt with soon.[19]

To conclude, declining fuel excise revenue is not necessarily the dire issue that it is sometimes made out to be, and a road user charge is not the only, or necessarily the most desirable, solution to this problem. Nonetheless, there are several other motivations for adopting a distance-based road user charge, including the fairness of our road taxation system with the uptake of electric vehicles. Other motivations which have not been discussed in this article include externality pricing – such as for congestions and emissions. Policy makers should consider the potential advantages of these approaches in the context of developing a road user charge for light vehicles. Charging systems to achieve each of these aims may be very different to those designed to address future infrastructure expenditure shortfalls.

It appears unlikely that Governments of any level will take immediate steps to implement a road user charge. At the recent federal election, neither road user charging for light vehicles nor fuel excise as a source of revenue was discussed directly, indicating that it is likely not a significant priority for either party. As noted earlier, a proposed study into light vehicle charging reform by the Commonwealth has not eventuated, with the Australian Financial Review reporting that this work has been cancelled. [20] To date, Commonwealth efforts on road user charging have been centered on heavy vehicle charges and related institutional reforms, hence it seems likely that this will continue, while light vehicle charging reform will take a back seat. State Governments have also not expressed interest in light vehicle charging reform, hence, it is unlikely that we will see a serious push to implement road user charging for light vehicles from governments in the near future. Even if we do, it is likely to take over ten years to implement. In short, it looks like fuel excise is likely here to stay – don’t expect to have to pay a distance-based charge any time soon.

[1] https://www.abc.net.au/news/2018-01-15/electric-cars-breaking-australia-roads-reform-road-user-charging/9235564

[2] https://www.afr.com/news/politics/deputy-pm-michael-mccormack-shelves-inquiry-into-road-pricing-20181004-h1688d

[3] https://minister.infrastructure.gov.au/pf/speeches/2016/pfs007_2016.aspx

[4] https://www.paulfletcher.com.au/portfolio-speeches/speech-to-launch-response-to-the-australian-infrastructure-plan-building-our

[5] https://transportinfrastructurecouncil.gov.au/publications/heavy_vehicle_road_reform.aspx

[6] And reportedly has been cancelled according to the Australian Financial Review, although the Government has not released any statements cancelling the study: https://www.afr.com/news/politics/deputy-pm-michael-mccormack-shelves-inquiry-into-road-pricing-20181004-h1688d

[7] https://minister.infrastructure.gov.au/pf/speeches/2016/pfs007_2016.aspx

[8] Australian Infrastructure Yearbook 2018, BITRE, Table T1.4a; https://bitre.gov.au/publications/2018/files/infrastructure-statistics-yearbook-2018.pdf

[9] For more info on fuel tax credits, see: https://www.ato.gov.au/business/fuel-schemes/fuel-tax-credits—business/

[10] ATO website: https://www.ato.gov.au/business/excise-and-excise-equivalent-goods/fuel-excise/excise-rates-for-fuel/

[11] Australian Infrastructure Yearbook 2018, BITRE, Tables T1.2d; T1.4a; T4.2; https://bitre.gov.au/publications/2018/files/infrastructure-statistics-yearbook-2018.pdf

[12]https://www.aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Library/pubs/rp/BudgetReview201415/FuelExcise

[13] Australian Infrastructure Yearbook 2018, BITRE, Table T1.4a; https://bitre.gov.au/publications/2018/files/infrastructure-statistics-yearbook-2018.pdf

[14] https://www.abc.net.au/news/2018-01-15/electric-cars-breaking-australia-roads-reform-road-user-charging/9235564

[15] https://www.afr.com/news/politics/deputy-pm-michael-mccormack-shelves-inquiry-into-road-pricing-20181004-h1688d

[16] https://grattan.edu.au/news/road-user-charging-belongs-on-the-political-agenda-as-the-best-answer-for-congestion-management/ “Linking fuel excise to road funding is a furphy and gets us onto the wrong track at the very start of the road-pricing journey. Fuel excise is merely one source of general government revenue and is not in any way hypothecated.”

[17] https://www.abc.net.au/news/2018-01-15/electric-cars-breaking-australia-roads-reform-road-user-charging/9235564

[18] The obvious response is to say that EVs have significant environmental benefits and hence those who drive them should get a tax concession. However, note that fuel excise is not calculated based on environmental cost and so offering a fuel excise discount/waiver may not accurately reflect the environmental benefit of an EV.

[19] https://www.afr.com/news/politics/national/if-electric-cars-are-in-the-fast-lane-their-drivers-must-pay-road-tax-20190401-p519nn

[20] https://www.afr.com/news/politics/deputy-pm-michael-mccormack-shelves-inquiry-into-road-pricing-20181004-h1688d